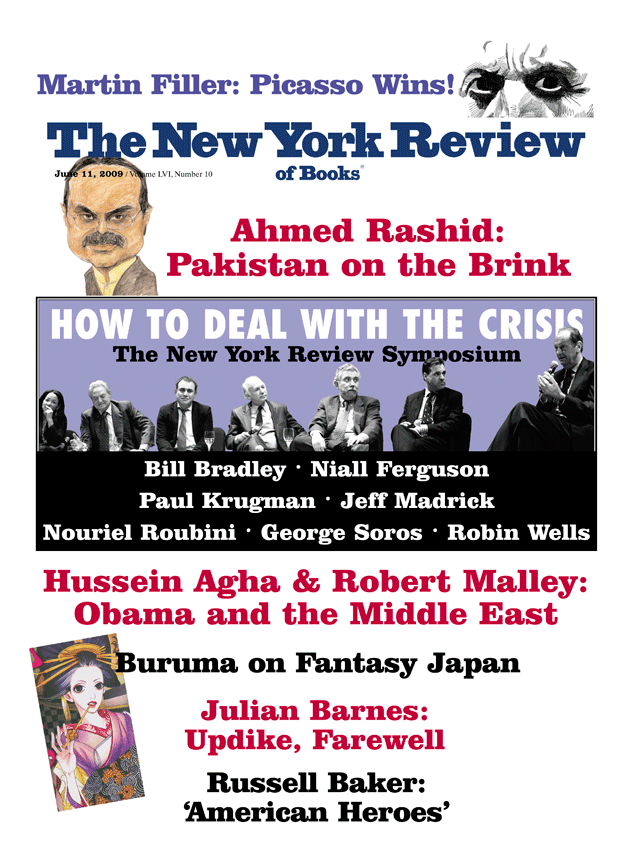

—The Editors

Jeff Madrick: It was six months ago now that the Lehman debacle occurred, that AIG was rescued, that Bank of America bought Merrill Lynch; it was about six months ago that the TARP funds started being distributed. The economy was doing fairly poorly in much of 2008, and then fell off a cliff in the last quarter of 2008 and into 2009, shrinking at a 6 percent annual rate—an extraordinary drop in our national income. It is now by some very important measures the worst economic recession in the post–World War II era. Employment has dropped faster than ever before in this space of time.

We have a three-front problem: a housing market that went crazy as the housing bubble burst; a credit crisis, the most severe we’ve known since the early 1930s; and now a sharp drop in demand for goods and services and capital investment, leading to a severe recession. What gives us the jitters is that all of these are related. We have seen some deceleration in the rate of economic decline, and many people are saying that “green shoots” are showing. What is the actual state of the economy, and do we need a serious mid-course correction on the part of the Obama administration?

Bill Bradley: How far are we along in a recovery? When the market price of Citicorp drops from 60 to 1, and then comes back to 3, I don’t think that’s a recovery. Warren Buffett buys Goldman Sachs, and after he buys, the price drops 45 to 50 percent, and if he’s going to break even on the investment he’s got to earn 9 percent for the next twelve years, I don’t think that’s a recovery. The administration has put in place measures that, if they were to work, could offer some hope.

What I’d like to suggest is that if they don’t work, there’s an alternative. The national government has now made about $12.7 trillion in guarantees and commitments to the US financial sector, and we’ve already spent a little over $4 trillion in this crisis. Some institutions such as Citicorp, for example, received about $60 billion in direct assistance, and $340 billion in guarantees. So US taxpayers are into Citicorp for around $400 billion. If we look out to June, July, and if we see that the PPIP [Public-Private Investment Program, created by Treasury Secretary Timothy Geithner] is not succeeding, that the bank assets aren’t being bought at levels that they should be bought from the books of banks, then there is an alternative.

Think back to Citicorp. I looked at the ticker today: the market capitalization of Citicorp is $17 billion. So the government could buy Citicorp for a fraction of what we’ve already obligated the taxpayer for. And in buying Citicorp, as an example—there could be one or two others—the government would announce in four to six months that it is going to sell the good assets of the bank back to the public. If the government bought Citicorp for, let’s say, $20 billion, what would it be worth if the government sold the good assets back to the public? Surely, several times what it paid for it.

I don’t mean selling these assets to hedge funds, although they can participate; but I would propose offering them to any American who wants to invest in this good bank the opportunity to do so.

The prospect of that happening would bring very strong, positive influence on the development of the whole economy. And what would the government then be left with? The bad bank—that is, the bad assets that we’re going through hoops now to try to get off the bank books. Instead the government would have those assets and it could take fifteen to twenty years to clean them up. So I say I would like to see the existing program work. But if it doesn’t work, there is an alternative, and it’s an alternative in the long run in which the average guy in America could participate.

Niall Ferguson: This is the end of the age of leverage, which began, I guess, in the late 1970s, and saw an explosive rise in the ratio of debt to gross domestic product, not only in this country, but in many, many other countries. Once you end up with public and private debts in excess of three and a half times the size of your annual output, you are Argentina. You know, it’s funny that people refer all the time back to the collapse of Lehman last September. Let’s remember that this crisis actually began in June 2007. It fully became clear in August of 2007 that major financial institutions were almost certainly on the brink of insolvency to anybody who bothered to think about the impact of subprime mortgage defaults on their balance sheets.

Advertisement

But we were in denial. And we stayed in denial until September, more than a year later, of last year. Then we had the breakdown. Notice how psychological terms are very helpful when economics fails as a discipline. After the breakdown, we came out of denial and we realized that probably more than one major bank was insolvent. Then in September and October the world went into shock. It was deeply traumatic.

Now we’re in the therapy phase. And what therapy are we using? Well, it’s very interesting because we’re using two quite contradictory courses of therapy. One is the prescription of Dr. Friedman—Milton Friedman, that is —which is being administered by the Federal Reserve: massive injections of liquidity to avert the kind of banking crisis that caused the Great Depression of the early 1930s. I’m fine with that. That’s the right thing to do. But there is another course of therapy that is simultaneously being administered, which is the therapy prescribed by Dr. Keynes—John Maynard Keynes—and that therapy involves the running of massive fiscal deficits in excess of 12 percent of gross domestic product this year, and the issuance therefore of vast quantities of freshly minted bonds.

There is a clear contradiction between these two policies, and we’re trying to have it both ways. You can’t be a monetarist and a Keynesian simultaneously—at least I can’t see how you can, because if the aim of the monetarist policy is to keep interest rates down, to keep liquidity high, the effect of the Keynesian policy must be to drive interest rates up.

After all, $1.75 trillion is an awful lot of freshly minted treasuries to land on the bond market at a time of recession, and I still don’t quite know who is going to buy them. It’s certainly not going to be the Chinese. That worked fine in the good times, but what I call “Chimerica,” the marriage between China and America, is coming to an end. Maybe it’s going to end in a messy divorce.

No, the problem is that only the Fed can buy these freshly minted treasuries, and there is going to be, I predict, in the weeks and months ahead, a very painful tug-of-war between our monetary policy and our fiscal policy as the markets realize just what a vast quantity of bonds are going to have to be absorbed by the financial system this year. That will tend to drive the price of the bonds down, and drive up interest rates, which will also have an effect on mortgage rates—the precise opposite of what Ben Bernanke is trying to achieve at the Fed.

One final thought: Let’s not think of this as a purely American phenomenon. This is a crisis of the global economy. I’d go so far as to say it’s a crisis of globalization itself. The US economy is not going to contract the most this year, even if the worst projections at the International Monetary Fund turn out to be right; a 2.6 percent contraction is far, far less than the shock already being inflicted on Japan, on South Korea, on Taiwan, to say nothing of the shock being inflicted on Europe. Germany is contracting at something close to 5 or 6 percent. So we are faced not just with a problem to be dealt with by American policy, we are faced with a crisis of global proportions, and it’s far from clear to me that the prescriptions of Dr. Friedman and Dr. Keynes together can solve that massive global crisis.

Paul Krugman: Let me respond to that a bit. Let’s think about what is actually happening to the global economy right now. On the one side there has been an abrupt realization by many people that they have too much debt, that they are not as rich as they thought. US households have seen their net worth decline abruptly by $13 trillion, and there are similar blows occurring around the world. So the people, individual households, want to save again. The United States has gone from approximately a zero savings rate two years ago up to about 4 percent right now, which is still below historical norms; but suddenly saving is occurring.

Advertisement

That saving ought to be translated into investment, but the investment demand is not there. Housing is flat on its back because it was overbuilt; housing bubbles collapsed not only in the United States, but across much of Europe. Many businesses cannot get access to capital because of the breakdown of the financial system. But even those that do have access to capital don’t want to invest because consumer demand is not there. Between the housing bust and the sudden decision of consumers to save, after all, we have a world with lots of excess capacity. The GDP report that just came out says that business-fixed investment, non-residential fixed investment, essentially business investment, is falling at a 40 percent annual rate.

This causes a problem. There are lots of people who want to save, creating a vast increase in savings, not only in the US but around the world, combined with a sharp decline in the amount that the private sector is willing to invest, even at a zero interest rate, or rather even at a zero interest rate for US government debt, which is what the Federal Reserve has the most direct impact on.

One way to think about the global crisis is a vast excess of desired savings over willing investment. We have a global savings glut. Another way to say it is we have a global shortage of demand. Those are equivalent ways of saying the same thing. So we have this global savings glut, which is why there is, in fact, no upward pressure on interest rates. There are more savings than we know what to do with. If we ask the question “Where will the savings come from to finance the large US government deficits?,” the answer is “From ourselves.” The Chinese are not contributing at all.

Now, the great concern I have is that although we understand these things fairly well, there are thirty-eight Republican senators who say that the answer for the crisis is another round of Bush-style tax cuts that will reduce revenues by $3 trillion over the next decade.

This crisis has been so large and the political process has been so sluggish that the difficulties have been greater than expected. And yes, there are some green shoots. Things are getting worse more slowly, but we have not managed to head off a crisis that could turn out to be self-reinforcing, and leave us in this trap for many, many years.

Nouriel Roubini: It’s pretty clear by now that this is the worst financial crisis, economic crisis and recession since the Great Depression. A number of us were worrying about it a while ago. At this point it’s becoming conventional wisdom.

The good news is probably that six months ago there was a risk of a near depression, but we have seen very aggressive actions by US policymakers, and around the world. I think the policymakers finally looked into the abyss: they saw that the economy was contracting at a rate of 6 percent–plus in the US and around the world, and decided to use almost all of the weapons in their arsenals. Because of that I think that the risk of a near depression has been somewhat reduced. I don’t think that there is zero probability, but most likely we are not going to end up in a near depression.

However, the consensus is now becoming optimistic again and says that we are going to go from minus 6 percent growth to positive growth in the second half of this year, meaning that the recession is going to be over by June. By the fourth quarter of 2009, the consensus estimates that growth is going to be positive, by 2 percent, and next year more than 2 percent. Now, compared to that new consensus among macro forecasters, who got it wrong in the past, my views are much more bearish.

I would agree that the rate of economic contraction is slowing down. But we’re still contracting at a pretty fast rate. I see the economy contracting all the way through the end of the year, going from minus 6 to minus 2, not plus 2. And next year the growth of the economy is going to be very slow, 0.5 percent as opposed to the 2 percent–plus predicted by the consensus. Also, the unemployment rate this year is going to be above 10 percent, and is likely to be close to 11 percent next year. Thus, next year is still going to feel like a recession, even if we’re technically out of the recession.

The outlook for Europe and Japan, both this year and next year, is even worse. Most of the advanced economies are going to do worse than the United States for a number of reasons, including structural factors in Japan and weak policy response in the case of the Euro zone.

The problems of the financial system are severe. Many banks are still insolvent. If you don’t want to end up like Japan with zombie banks, it’s better, as Bill Bradley suggested, to do what Sweden did: take over the insolvent banks, clean them up, separate good and bad assets, and sell them back in short order to the private sector.

Now, on the question of policy responses, there is no inconsistency between monetary easing and fiscal easing. Both of them should be stimulating demand, and the monetary easing should be leading also to restoration of credit. Of course, in a situation in which the economy is suffering not just from a lack of liquidity but also problems of solvency and a lack of credit, traditional monetary policy doesn’t work as well. You also have to take unconventional monetary actions, and you have to fix the banks. And we need a fiscal stimulus because every component of our economy is sharply falling: consumption, residential investment, nonresidential construction, capital spending, inventories, exports. The only thing that can go up and sustain the economy for the time being is the fiscal spending of the government.

However, fiscal policy cannot resolve problems of credit, and it is not without cost. Over the next few years it’s going to add about $9 trillion to the US public debt. Niall Ferguson said it’s the end of the age of leverage. It’s not really. There is not deleveraging. We have all the liabilities of the household sector, of the banks and financial institutions, of the corporate sectors; and now we’ve decided to socialize these bad debts and to put them on the balance sheet of the government. That’s why the public debt is rising. Instead, when you have an excessive debt problem, you have to convert such debt into equity. That’s what you do with corporate restructuring—it converts unsecured debt into equity. That’s what you should do with the banks: induce the unsecured creditors to convert their claims into equity. You could do the same thing with the housing market. But we’re not doing the debt-into-equity conversion. What we’re doing is piling public debt on top of private debt to socialize the losses; and at some point the back of some governments’ balance sheet is going to break, and if that happens, it’s going to be a disaster. So we need fiscal stimulus in the short run, but we have to worry about the long-run fiscal sustainability, too.

George Soros: There are two features that I think deserve to be pointed out. One is that the financial system as we know it actually collapsed. After the bankruptcy of Lehman Brothers on September 15, the financial system really ceased to function. It had to be put on artificial life support. At the same time, the financial shock had a tremendous effect on the real economy, and the real economy went into a free fall, and that was global.

The other feature is that the financial system collapsed of its own weight. That contradicted the prevailing view about financial markets, namely that they tend toward equilibrium, and that equilibrium is disturbed by extraneous forces, outside shocks. Those disturbances were supposed to occur in a random fashion. Markets were seen basically as self-correcting. That paradigm has proven to be false. So we are dealing not only with the collapse of a financial system, but also with the collapse of a worldview.

That’s the situation that President Obama inherited. He’s faced with two objectives. One, he must arrest the collapse and, if possible, reverse it. Second, he has to reconstruct the financial system because it cannot be restored to what it was. This is a new situation. When people see this crisis as being the same as previous financial crises, they’re making a mistake.

The interesting thing is that what needs to be done in the short term is almost exactly the opposite of what needs to be done in the long term. Obviously the problem was excessive leverage. But when you have a collapse of credit there’s only one source of credit that is still credible, and that’s the state: the Federal Reserve and the Treasury. Then you have actually to inject a lot more leverage and money into the economy; you have to print money as fast as you can, expand the balance sheet of the Federal Reserve, increase the national debt. And that is, in fact, what has been done, which is the right thing to do. But then once this policy is successful, you have to rein in the money supply as fast as you can.

I would say that policy has generally lagged behind events. We were behind the curve. Now that the free fall is moderating, and the collapse has more or less occurred, I think there is hope that policy will, in fact, catch up with events. The outcome of the stress test of the banks will be important, because that’s basically where the policy has been lagging behind—in recapitalizing the banks. And that’s where most of the confusion comes from.

Robin Wells: I want to go back to what Paul said about the global savings glut. The global savings glut is what drove interest rates down to historically low levels. Housing is very sensitive to the interest rate, and therefore a housing bubble was practically foreordained by an extended period of low interest rates. But you’ll also notice that the bubble in housing hasn’t occurred just in the United States, it’s also occurred in Spain, Eastern Europe, and the UK; it’s been in Ireland, it’s been in Iceland. In order to prevent us from reexperiencing this catastrophe in another, say, ten years, we need to look at the origins of the global savings glut. Yes, there are some differences in how the bubbles were actually manifested in the different countries, and those manifestations are important; but let’s look for a moment at the global savings glut in its entirety.

I think this story starts really in the Eighties. During the Reagan years, we experienced chronic fiscal deficits, and we began to abdicate our responsibility to raise tax revenue that could sustainably finance government. In order to do that, we had to borrow, and who did we borrow from? We borrowed from countries that were running persistent trade surpluses. And as we continued to run these deficits with these countries, there grew to be a symbiotic relationship, as Niall Ferguson says, this Chimerica.

But it was on several different fronts. There were the net exporters, such as China, Japan, and Germany, and the net importers of capital, the largest, of course, being the United States. This import of capital allowed us to consistently live beyond our means, first by running fiscal deficits, not raising enough tax revenue to finance the government, and then also through, ultimately, the leverage that we used in housing, and in commercial real estate, and in leverage buyouts. And this continued; it grew because there was no point anywhere along the line at which anyone would say “halt.”

The persistent imbalances led us to pretend that we could keep borrowing without having sufficient tax revenue to pay for the government. And if your house prices are rising, if the stock market is going up—which of course is going to happen if you have cheap money—it puffs up the value of the assets, and disguises a lot of other structural problems such as rising inequality and corruption.

With this inflow of capital from abroad, the financial sector in the United States also became larger and larger relative to the rest of the economy, with GDP tilted disproportionately toward the financial sector.

How do we start to get out of this? In many ways we’re almost adverse to bringing up the situation in which we find ourselves with the net exporting countries. I thought it was quite interesting a few weeks ago when many Chinese officials were saying that it was proper, and it was good economically, that the US continue to run persistent trade imbalances with China, that the Chinese yuan did not need to be appreciated, that we should continue doing the things we always have, and that the US should make sure that the value of Chinese assets were not diminished by any change in the value of the dollar. It should have been clear that this was not a sustainable relationship, but no one was willing to say that.

So I think we’re going to have to address these chronic global trade imbalances. You might very well see a shift toward more protectionism. We’re going to have to actually do something about raising taxes so that we can sustain government from our own resources rather than depending upon borrowing abroad. And we’re going to have to start stepping back into our former role, one that we abdicated, as managers and guardians in the global economy.

J.M.: I think most people think the US government did what it had to in adopting a serious stimulus, despite the debt. Niall, why don’t you respond to the comments, and then we’ll have a little discussion on that.

N.F.: Well, if you listened carefully to what Paul Krugman said, he actually agreed with me. Because what he said was that everything is just fine as long as the financial credibility of the United States isn’t called into question, but my point is that it will be called into question. Of course it will. According to the administration’s crazily optimistic forecast for a recovery, it’s going to be a 3 percent growth rate next year, 4 percent the year after that, 4.6 percent the year after that. If you believe those numbers, you’ll believe absolutely anything, but they are there in the administration’s budget document. Even if those numbers turn out to be true, the federal debt will rise over the next five to ten years to around 100 percent of gross domestic product.

But since those numbers are clearly wrong, and the trend growth rate of the US will be much closer to 1 percent than to 4, it seems reasonable to anticipate a much more rapid explosion of federal debt to somewhere in the region of 140 or 150 percent of gross domestic product. Even if the private savings rate rebounded to its highest point in the postwar period, it would still account for no more than 5 percent of gross domestic product. But this year’s deficit, as I said earlier, is likely to be north of 12 percent of gross domestic product. So it doesn’t quite add up.

The Fed has committed itself to buying $300 billion worth of treasuries this year, but clearly it will have to buy a great many more than that. Remember, $1.7 trillion or so are coming onto the market. And you assume that the credibility of the United States in the eyes of Americans, as well as foreign investors, is going to withstand this? At some point the United States does start to look like a Latin American economy, not only to people abroad but maybe to people at home. If the Fed’s balance sheet explodes to up to $3 or $4 trillion, who knows how big it could get. At what point do people stop believing in the US dollar as a reserve currency, or even as a store of value for their own savings?

J.M.: Let’s allow Paul and others to respond.

P.K.: The essence of this kind of recession is precisely that the amount that collectively we want to save is greater than the amount that collectively we want to invest. That is the problem. You can’t get around that.

There is a very different question, which is the long-run solvency of the US government, and I do worry about that. I would disagree very much with Niall about those numbers, but this is a factor that should be taken into account. We are currently in debt about 60 percent of GDP. We have in the past been as high as 100 percent of GDP at the end of World War II without having a crisis, but your ability to go that high does depend upon people’s belief that you will behave responsibly, and that is somewhat in question. I hope it is less in question than it was in the past, now that we’ve had some regime changes, but it is a problem.

N.R.: I think that the debate here is about what needs to be done in the short term versus the long term. The lesson of the Great Depression is pretty clear: it started with the stock market crash of 1929, and it actually became the Great Depression by 1933 for four reasons. One, we didn’t believe in a counter-cyclical monetary policy. The money supply contracted rather than being eased. Interest rates were not falling, and that made the credit crunch worse. Two, nobody believed in counter-cyclical fiscal policy. The general theory of Keynes was written only in 1936; in the early 1930s, the government was raising taxes and cutting spending in order to maintain a balanced budget. That made the recession even more severe.

Three, there was a belief that banks should be allowed to collapse. Thousands of them collapsed, the credit crunch became even worse. And four, by 1933, 75 percent of households had defaulted on their mortgages; they couldn’t pay them. So a stock market crash became a Great Depression. Then you add currency wars internationally, trade wars, protectionism, and capital controls; then you had default by countries and the rise of totalitarian regimens in Germany and in Italy, in Japan, and Spain, and we ended up in World War II. So those are the consequences of not taking the right policy actions in the short run.

I agree, however, that we have to worry about the long run. If we’re going to finance budget deficits by printing money, we may have high inflation, even risk of hyperinflation in some countries. That’s what happened in Germany in the 1920s during the Weimar Republic. We are having large budget deficits and increasing the public debt, we don’t know whether it’s going to be $5 trillion or $10 trillion of more debt. But there are only a few ways of resolving that debt problem: either you default on it as countries like Argentina did; or you use the inflation tax to wipe out the real value of the debt; or you have to raise taxes and cut government spending. And given the size of the deficits, over time that’s going to be a painful political choice to make. So we need the stimulus in the short run, but we need to restore medium-term fiscal sustainability.

G.S.: Let’s face it, for twenty-five years we have been consuming more than we have been producing. This living beyond our means accumulated mainly in the housing sector and the financial sector, and now those liabilities are being nationalized. It’s a bit unfortunate that so far we have only nationalized the liabilities of the banks, and not their assets. I think it’s right that we are extending a government credit to replace the collapsing credit, and we are currently in a deflationary situation. When the flow of credit restarts, suddenly there will be a flip-flop where the fear of deflation will be replaced by the fear of inflation. The pressure for interest rates to rise will be very, very strong, and the rise in interest rates could choke off the recovery. And so we are facing a period of stop-go, or stagflation similar to but more severe than what we faced in the Seventies. But that is a favorable outcome compared to what would have happened if we hadn’t done what we are doing.

About regulation, we have to start by recognizing that the prevailing view is false, that markets actually are bubble-prone. They create bubbles. Therefore, they have to be regulated. The authorities have to accept responsibility for preventing asset bubbles from growing too big. They’ve expressly rejected that, saying that if the markets don’t know, how can the regulators know? And, of course, they can’t. They’re bound to be wrong, but they get feedback from the market, and then they can make adjustments. Now, it is not enough to regulate the money supply. You have to regulate credit. And that means using tools that have largely fallen into disuse. Of course you have margin requirements, minimum capital requirements; but you actually have to vary them to counteract the prevailing mood of the market, because markets do have moods. It should be recognized that exuberance actually is quite rational. When I see a bubble beginning, forming, I jump on it because that’s how I make money. So it’s perfectly rational.

It’s the job of the regulators to regulate. However, we should try not to go overboard. While markets are imperfect, regulators are even more imperfect: not only are they human, they’re also bureaucratic and subject to political influences. So we want to keep regulation to a minimum, but we have to recognize that markets are inherently unstable.

N.R.: On this question of regulation, of course, we go into cycles, you know. We had the Great Depression, and then we imposed many actually useful regulations, both on the financial system and on the real economy. Some of them became excessive, and even before Reagan and Thatcher, Jimmy Carter started deregulating some parts of the economy. Eventually policy makers started believing that self-regulation is best; but that means no regulation. We believed in market discipline; but there is no discipline when there is irrational exuberance. We relied on internal risk management models; but nobody listened to risk managers when the risk takers were making all the profits in the banks; and we relied on rating agencies which had massive conflicts of interest since they were being paid by those that they were supposed to be rating. So the entire model of self-regulation and market discipline now has collapsed.

We have to go to a world where there is greater prudential regulation and supervision of the financial system. I think the challenge for the US economy is, can we grow without excessive credit and leverage? Can we grow in a more sustainable way? And what are going to be the sectors of the economy that give us sustainable, long-term growth? I think that’s an open question.

P.K.: I think there are two big structural changes that we’d want to see. One is we need to reduce the role of the financial sector in the economy. We went from an economy in which about 4 percent of GDP came from the financial sector to an economy in which 8 percent of GDP come from the financial sector, and in which at its peak 41 percent of profits were being earned by the financial sector. And there is no reason to believe that anything productive happened as a result of all of that. These extremely highly compensated bankers were essentially just finding new ways to offload risks on to other people.

As I’ve written, we need a boring banking sector again. All of this high finance has turned out to be just destructive, and that’s partly a matter of regulation. But in the political economy there was also a vicious circle. Because as the financial sector got increasingly bloated its political clout also grew. So, in fact, deregulation bred bloated finance, which bred more deregulation, which bred this monster that ate the world economy.

The other thing not to miss is the importance of a strong social safety net. By most accounts, most projections say that the European Union is going to have a somewhat deeper recession this year than the United States. So in terms of macromanagement, they’re actually doing a poor job, and there are various reasons for that: the European Central Bank is too conservative, Europeans have been too slow to do fiscal stimulus. But the human suffering is going to be much greater on this side of the Atlantic because Europeans don’t lose their health care when they lose their jobs. They don’t find themselves with essentially no support once their trivial unemployment check has fallen off. We have nothing underneath. When Americans lose their jobs, they fall into the abyss. That does not happen in other advanced countries, it does not happen, I want to say, in civilized countries.

And there are people who say we should not be worrying about things like universal health care in the crisis, we need to solve the crisis. But this is exactly the time when the importance of having a decent social safety net is driven home to everybody, which makes it a very good time to actually move ahead on these other things.

N.F.: Well, I tell you what, I feel depressed after what I’ve heard tonight. We are now contemplating a massive expansion of the state to substitute for the private sector because that’s the only thing Paul thinks will deliver growth. We’re going to reregulate the markets, we’re going to go back to those good old days. Where were you in the 1970s when all these wonderful regulations were in place? I don’t remember that going too smoothly. But what else are we going to do? We’re going to print money. Almost limitlessly we’ll print money. That’s going to be fine, too. And when we’re done with that, we’re going to raise taxes. What a fabulous package we have in store for us. You know, back in late 2007, I was asked what my big concern was, and I said, “My concern is that we’re going to get the 1970s for fear of the 1930s.” It’s very easy to forget, in your iron indignation at the failure of the market, where the true mainsprings of economic growth lie. The lesson of economic history is very clear. Economic growth does not come from state-led infrastructure investment. It comes from technological innovation, and gains in productivity, and these things come from the private sector, not from the state.

B.B.: As we look at the future, we also have to look at the mistakes policymakers made in the last ten years. It’s not news that people are greedy. But we made conscious decisions not to put limits on that natural human impulse. What were the mistakes? In 1999, we allowed investment banks, banks, insurance companies to combine: we eliminated the Glass-Steagall Act, which prohibited commercial banks from operating as investment banks. Why was Glass-Steagall put into law? Because the last time we didn’t limit greed we got into trouble, the Great Depression.

The second mistake was in 1999, the explicit decision by the Clinton administration and Congress not to regulate derivatives, in particular credit default swaps. In 2002 they were worth $1 trillion and today they’re worth $33 trillion, and that decision not to regulate derivatives created the following sequence: you have mortgages; then a thousand mortgages are packaged and sold as a mortgage-backed security; a thousand mortgage-backed securities are packaged and sold as a collateral debt obligation [CDOs]; then a thousand collateral debt obligations are packaged and sold as a CDO squared; and insuring each one of those bundles are credit default swaps, which are a part of that $33 trillion. And our government deliberately decided not to regulate this chain of investments.

One result was that the 374 people in the London office of AIG who were responsible for AIG derivatives destroyed a company that had 116,000 employees in 120 countries. Why? Because there was no regulation at all.

The third decision was in 2004. The SEC allowed banks to go from 10 to 1 leverage to 30 to 1 leverage. And guess what? Once they were allowed to do it, they did it. So if we’re going to look at the future, we might think of undoing those three mistakes.

Finally, we might want to remember that the chairman of the Federal Reserve is supposed to remove the punch bowl from the party when the party gets out of control. And that did not happen in the Greenspan years. The opposite happened.

This Issue

June 11, 2009

Pakistan on the Brink

Obama and the Middle East

This Issue

June 11, 2009

Pakistan on the Brink

Obama and the Middle East

{kind=link}

{kind=link}