Very few economists foresaw the great recession of 2008–2009. Why not? Economists have long assumed that human beings are “rational,” but behavioral findings about human fallibility have put a lot of pressure on that assumption. People tend to be overconfident; they display unrealistic optimism; they often deal poorly with risks; they neglect the long term (“present bias”); and they dislike losses a lot more than they like equivalent gains (“loss aversion”). And until recent years, most economists have not had much to say about the problem of inequality, which seems to be getting worse.

There is a strong argument that within the economics profession, these problems are closely linked, and that they have had unfortunate effects on public policy. Most economists celebrate free markets, invoking the appealing idea of consumer sovereignty. If people are buying potato chips, candy, and beer, or making risky investments, that’s their business; they know their own values and tastes. Outsiders, and especially those who work for the government, have no right to intervene. To be sure, things are different if someone is inflicting harms on third parties. If a company is emitting air pollution, the government can legitimately respond. But otherwise, many economists tend to believe that people should fend for themselves.

It is true that companies might try to take advantage of consumers and investors, perhaps with outright lies, perhaps with subtler forms of deception, perhaps by manipulating their emotions. But from the standpoint of standard economic thinking, that’s nothing to panic about. The first line of defense is competition itself—and the market’s invisible hand. Companies that lie, deceive, and manipulate people are not going to last long. The second line of defense is the law. If a company is really engaging in fraud or deception, government regulators might well get involved, and customers are likely to have a right to compensation. But for economists, competitive markets are generally trustworthy, and so the old Latin phrase retains its relevance: caveat emptor.

By emphasizing human fallibility, the group of scholars known as behavioral economists has raised a lot of doubts about this view. Their catalog of errors on the part of consumers and investors can be taken to identify a series of “behavioral market failures,” each of them calling for some kind of government response (such as information campaigns to promote healthy eating or graphic warnings to discourage smoking). But George Akerlof and Robert Shiller want to go far beyond behavioral economics, at least in its current form. They offer a much more general, and quite damning, account of why free markets and competition cause serious problems.

Both Akerlof and Shiller have won the Nobel Prize; they rank among the most important economists of the last half-century. They are also intellectual renegades. Akerlof has been interested in the persistence of caste systems, involuntary unemployment, rat races, the effects of personal identity, and what happens when sellers know things that buyers don’t. He has long been a proponent of integrating psychology and economics. A specialist in the financial system, Shiller has explored the role of “irrational exuberance” in producing wildly inflated stock, bond, and real estate prices, which are bound to come down. He believes that investors make serious mistakes, and also that they run in herds, which can produce bubbles. Like Akerlof, he is keenly interested in seeing what psychology can add to economic theory.

Akerlof and Shiller believe that once we understand human psychology, we will be a lot less enthusiastic about free markets and a lot more worried about the harmful effects of competition. In their view, companies exploit human weaknesses not necessarily because they are malicious or venal, but because the market makes them do it. Those who fail to exploit people will lose out to those who do. In making that argument, Akerlof and Shiller object that the existing work of behavioral economists and psychologists offers a mere list of human errors, when what is required is a broader account of how and why markets produce systemic harm.

Akerlof and Shiller use the word “phish” to mean a form of angling, by which phishermen (such as banks, drug companies, real estate agents, and cigarette companies) get phools (such as investors, sick people, homeowners, and smokers) to do something that is in the phisherman’s interest, but not in the phools’. There are two kinds of phools: informational and psychological. Informational phools are victimized by factual claims that are intentionally designed to deceive them (“it’s an old house, sure, but it just needs a few easy repairs”). More interesting are psychological phools, led astray either by their emotions (“this investment could make me rich within three months!”) or by cognitive biases (“real estate prices have gone up for the last twenty years, so they’re bound to go up for the next twenty as well”).

Advertisement

Akerlof and Shiller are aware that skeptics will find their depiction of human beings as “phools” to be inaccurate and impossibly condescending. Their response is that people are making a lot of bad decisions, producing outcomes that no one could possibly want. In their view, phishing for phools “is the leading cause of the financial crises that lead to the deepest recessions.” A lot of people run serious health risks from overeating, tobacco, and alcohol, leading to hundreds of thousands of premature deaths annually in the United States alone. Akerlof and Shiller think that it is preposterous to believe that these deaths are a product of rational decisions. Many people face debilitating financial insecurity, largely as a result of their own mistaken decisions, spurred by phishermen. Bad government is itself a product of phishing and phoolishness, for “we are prone to vote for the person who makes us the most comfortable,” even when that person’s decisions are effectively bought by special interests.

In a reversal of Adam Smith, Akerlof and Shiller contend that the invisible hand of the market guarantees phishing. Consider Cinnabon, whose brilliant motto is “Life Needs Frosting,” and which attracts customers with a seductive smell (and which has not made caloric information on its products at all easy to find). Or consider health clubs, a $22 billion industry with over 50 million customers, many of whom choose expensive monthly contracts, even though they would save a lot of money if they paid by the visit. In effect, they are paying not to go to the gym.

With reference to such examples, Akerlof and Shiller suggest that people can be imagined to have two kinds of tastes: those that would really make their lives better, and those that determine how they actually choose. In their view, the latter—influenced by a kind of “monkey-on-the-shoulder” who makes bad choices—often prevails. The problem is that as if by an invisible hand, companies “out of their own self-interest will satisfy those monkey-on-the-shoulder tastes.”

To support this claim, Akerlof and Shiller point to an uncanny prediction by John Maynard Keynes in 1930. Keynes expected that by 2030, the standard of living would be eight times higher. We are on track to get in that vicinity. At the same time, Keynes made a profound mistake. He predicted that the workweek would plummet to fifteen hours and that people would struggle not with financial problems, but with a surfeit of leisure. That isn’t going to happen. What Keynes missed is that free markets generate new desires. In Akerlof and Shiller’s words, markets “do not just produce what we really want; they also produce what we want according to our monkey-on-the-shoulder tastes.”

Phishermen know how to give rise to temptations, thus generating novel “needs.” For any human weakness, the invisible hand will produce phishermen, who will exploit phools—which means that long working hours, and difficulties in making ends meet, will continue to be with us even if the standard of living goes up eight times again (and then again).

Akerlof and Shiller contend that an understanding of phishing and phoolishness helps to explain the financial crisis of 2008–2009. In their account, the origins of the crisis lay in “the subversion of the system for rating fixed-income securities” such as bonds. For a long time, the public consulted the ratings of securities by US credit agencies in order to assess their likelihood of default. Until the 1990s, those ratings could be trusted. One reason is that securities were simple to assess. Another is that credit agencies avoided any conflict of interest. But when those agencies took on the task of rating bafflingly complex securities, above all financial derivatives, investors were no longer in a position to know whether the agencies continued to be worthy of trust. Around the same time, serious conflicts of interests emerged, as credit agencies began to charge investment banks for their ratings. As the banks ended up paying the raters’ bills, the ratings could no longer be trusted. But because ratings had been reliable in the past, investors thought they continued to be reliable.

Although investors were being phished, they “had no reason to be suspicious. They had been told of the wonders of free markets.” But free markets were not so wondrous, because they put the producers of the new, complex, risky securities at a big advantage over the producers of the older, simpler, safer ones. After all, the new securities promised higher returns while disguising the risk of default:

As long as a significant part of the bond-buying public was willing to swallow the myth whole, the investment bankers had an incentive to produce those rotten avocados, and to extract from the agencies the high ratings that would be the cover-up.

When the risk materialized, the whole system fell apart. (In this book, they do not emphasize the problem of subprime mortgages, which Shiller has explored elsewhere, and which also involved plenty of phishing.)

Advertisement

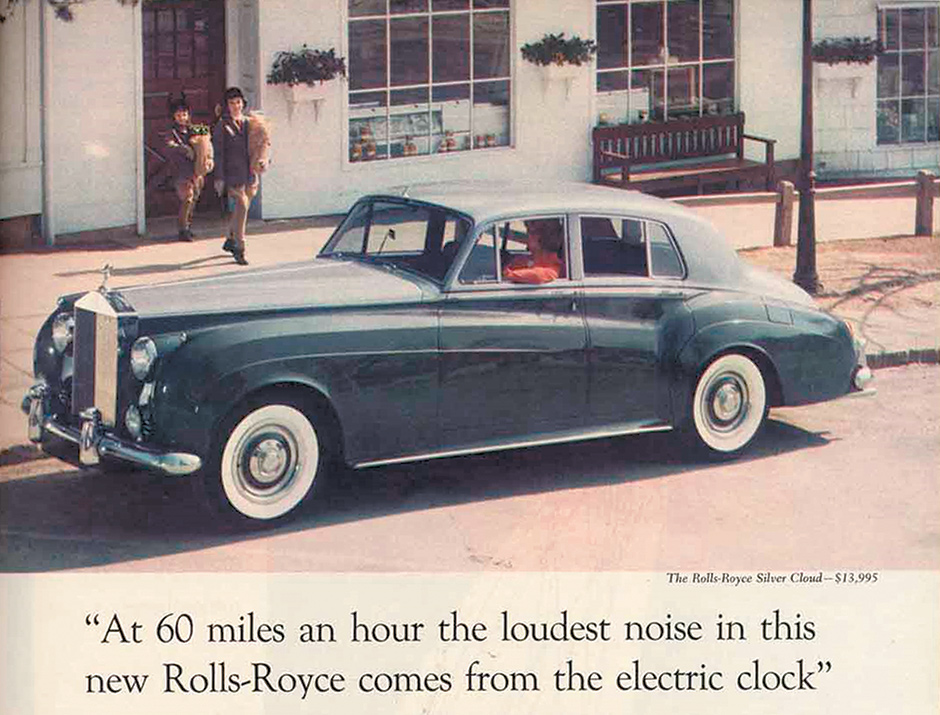

Akerlof and Shiller think that the idea of phishing also helps to explain modern advertising, especially when we focus on the crucial role of narrative in human thinking. Clever marketers offer simple, attractive stories about their products, and get those stories to stick in the human mind. Consider a famous advertisement for Rolls-Royce, displaying an elegant young mother in the driver’s seat, turned slightly toward her elegant children, who are walking toward the car from outside the entrance to an elegant grocery store. The headline of the copy: “At 60 miles an hour the loudest noise in this new Rolls-Royce comes from the electric clock.” Advertisements of this kind tell an appealing story about what life would be like with the product.

Akerlof and Shiller contend that presidents are sold in essentially the same way, as “modern statistical techniques now tell marketers and advertisers—both private and political—when and how to phish, just as modern techniques in geology tell the oil and gas companies where and how to drill.” They single out the 2012 Obama campaign for its use of statistical testing “as a new art form.” In their view, campaigns now know how to target “voters individual-by-individual,” with the help of modern statistical techniques. We should expect more such targeting in 2016.

Akerlof and Shiller contend that the invisible hand guarantees “rip-offs,” which are “fertile ground to find phishing for phools.” At the closings of home sales, for example, people face a baffling array of transaction costs. Real estate brokers’ fees usually run to 6 percent, and they are often higher. These and other costs are imposed after most buyers have made their decisions and are in no position to bargain. Akerlof and Shiller are also concerned that people spend a lot more money with credit cards than they do with cash. Sellers allow customers to use their cards for free, and do not charge them the fees on sales that they pay to the credit card companies. For many customers, the use of credit cards turns out to be a genuine problem, not least because they end up spending significant amounts on late fees and interest on unpaid balances. As it turns out, credit cards are “a major cause of personal bankruptcy,” leading Akerlof and Shiller to conclude “if credit cards are not phishing for phools, the companies who purvey them should tell it to the judge.”

Why do so many people smoke and drink? As early as the late 1940s, scientists were finding an association between smoking and lung cancer, to which the tobacco companies, acting as phishermen, responded with a specific strategy, which was to sow doubt. They “knew they could find other ‘scientists’ (especially among smokers) who would strongly voice the opinion that there was no ‘proven’ link between smoking and cancer.” The result of their efforts was to insinuate an influential “new story into the relationship between smoking and health,” one that emphasized a serious “scientific controversy.” (Climate change, anyone?) That story eventually failed, but it took decades, and even now, almost 18 percent of adults are smokers.

Akerlof and Shiller believe that the harms of alcohol are greatly underappreciated. They think that those harms “could be comparable to the harms from cigarettes, affecting not just 3 or 4 percent of the population, as a chronic life-downer [i.e., cause of a shortened life], but, rather, affecting 15 to 30 percent; the higher number especially if we also include the alcoholics’ most affected family members.” Akerlof and Shiller assemble suggestive evidence that alcohol consumption does far more damage to health than we think. Their larger theme is that “alcohol studies remain largely underfunded,” and without the necessary research, “we are especially prone to be phished for phools, since we cannot know whether we have the right story.” In their view, significant federal tax increases on ethanol (the kind of alcohol in alcoholic drinks) could have major health benefits—but the industry has successfully worked to prevent any such increases.

Akerlof and Shiller make related arguments about the marketing of pharmaceuticals (with reference to the Vioxx scandal), the success of Facebook (which, they argue, is a mixed blessing for young people in particular), the sale of junk bonds, and the democratic process. With respect to the latter, they are concerned about a clever electoral strategy commonly used to hook “phishable voters.” With this strategy, politicians endorse policies that “appeal to the typical voter on issues that are salient to her, and where she will be informed,” while also adopting a “stance that appeals to donors” on issues on which the typical voter is uninformed. Because of the largely unregulated system for corporate donations, lobbyists can enjoy spectacular returns, as when they give money with the hope of extracting votes, or favors, on high-stakes issues (such as regulation of savings and loan companies or highly technical tax questions) that are too complex to attract the attention of most voters.

From all of these examples, Akerlof and Shiller offer a general account, which is that phishing occurs because of the “manipulation of focus.” Like magicians and pickpockets, phishermen are able to take advantage of “an errant focus by the phool.” Indeed, the idea that free markets work, and that government is the problem, “is itself a phish for phools,” a kind of story, one that does not capture reality. With respect to Social Security reform, securities regulation, and campaign finance reform, the United States has suffered from false and skewed claims that fail to account for the fact that free markets make people free not only to choose but also “free to phish, and free to be phished. Ignorance of those truths is a recipe for disaster.”

Akerlof and Shiller contend that behavioral economists have failed to explore, or perhaps even to see, the ubiquity of phishing, and the extent to which free markets promote it. Instead of a catalog of human errors and behavioral biases, they seek a more general account, one that gives “a picture to the mental frames that inform people’s decisions.” That picture involves “the stories we are telling ourselves.” Akerlof and Shiller believe that the idea of storytelling is “a new variable” for economics, one that explains why “people make decisions that can be quite far from maximizing their own welfare.” Thus “phishing for phools is not some occasional nuisance. It is all over the place.” Whenever “we have a weakness—if we have a way in which we are phishable—the phishermen will be there in waiting.”

Akerlof and Shiller make a convincing argument that phishing occurs because of the operation of the invisible hand, not in spite of it. If a company can make money by deceiving or manipulating people, someone is going to create such a company, and it will prosper (unless the law regulates it). And if it prospers, companies that do not deceive or manipulate people may well be at a competitive disadvantage. Of course there are a lot of consumers out there, and some of them will avoid phishermen. In fact markets might well be segmented into sophisticates and phools, with the former avoiding, and the latter flocking to, complex (but risky) financial products, expensive closing fees, tobacco, and alcohol. Indeed it would be most accurate to point to a continuum of consumers and investors, with varying degrees of susceptibility to deception and manipulation. Akerlof and Shiller are certainly right to say that phishing can be profitable.

At the same time, there is a lot of vagueness in that idea. One way to clarify it would to isolate the behavioral biases that phishermen might exploit. Drawing on empirical findings, we could speak of optimistic phools, overconfident phools, loss-averse phools, inattentive phools, and present-biased phools, and ask how numerous they are, and examine whether and under what conditions companies are able to take advantage of them. But as we have seen, Akerlof and Shiller want to go beyond a catalog of behavioral biases in favor of “a very general way to describe the mental frames that underlie people’s decisions,” one that emphasizes the stories people tell themselves.

Such stories are undoubtedly important, but here is a possible objection. For social scientists, it is essential to come up with testable hypotheses. For example, economists hypothesize that when the price of a particular good increases, people will buy less of it. Behavioral economists also claim to have tested, and demonstrated, the existence of biases. For example, they say they have found that consumers’ decisions are more affected by a small tax (a loss) than a small subsidy (a gain), and that teachers perform better when employers threaten them with a loss than when they promise them a bonus. No one should doubt that people are influenced by the stories that they tell themselves, as the authors claim. But is that a testable hypothesis? Does it lead to distinctive predictions, which can be shown to be right or wrong?

It is arresting to speak of “phishermen” and “phools,” but Akerlof and Shiller would surely agree that when people make decisions that are questionable, or that go badly wrong, they might not be phools. Consumers might greatly enjoy wine, cheese, candy, and ice cream, and even if these choices turn out to be unhealthy, we need not speak of either phishing or phools. And Akerlof and Shiller would not disagree with the proposition that many people practice self-control when it comes to possible dangers, and when they do, their choices may be highly informed. Such people may be difficult to phool.

Separate treatment is required for cases of fraud and deception, as where sellers are untruthful about what they are selling, or fail to disclose relevant facts. If a company falsely tells people that a new drug will cure cancer, we have a case of fraud, and if it fails to inform people that a side effect of the drug is neurological damage, it is fair to speak of deception.

Akerlof and Shiller might have limited their analysis to the economics of fraud and deception, urging that the categories should be broadened to include (for example) complex financial products that carry serious risks that investors are unable to understand. How helpful is it to speak of phishing and phools? One answer is that Akerlof and Shiller want to go well beyond fraud and deception to capture all cases in which sellers successfully market goods to buyers who do not benefit from the transaction. They do not spend a lot of time unpacking the idea of “manipulation,” but they appear to be speaking of people who can be phished because sellers are able to take advantage of their emotions or their cognitive biases, thus leading to transactions that are not in buyers’ interests.

This is a promising idea, and to make progress on it, it is probably best to be quite specific. Emotions do not always lead consumers astray; people might know that they will love using a gorgeous new computer, eating a piece of chocolate cake (or two), and driving a fast new car. (Life does need frosting.) With respect to cognitive biases, the problem of high closing costs (which involves the difficulty of handling complexity) is different from that of tobacco consumption (which involves addiction and unrealistic optimism), and both of these are different from the problem of excessive use of credit cards (which involves bias toward the present and neglect of cumulative costs). Once we make such distinctions, we might end up speaking not of phishing in general, but of specific behavioral failures, and seeking remedies that are well suited to each.

In his great marginalia to Sir Joshua Reynolds’s Discourses, William Blake wrote, “To Generalize is to be an Idiot. To Particularize is the Alone Distinction of Merit.” Blake exaggerated, of course, and Akerlof and Shiller are the furthest thing from idiots; their extraordinary book tells us something true, and profoundly important, about the operations of the invisible hand. But the largest views can lose focus. If we seek to understand how the invisible hand goes wrong, and whether some kind of intervention is required, there is a lot to be said for specifying mechanisms and testing concrete hypotheses. If we do that, we might go far beyond a mere list, and we will find phishing of many different kinds.