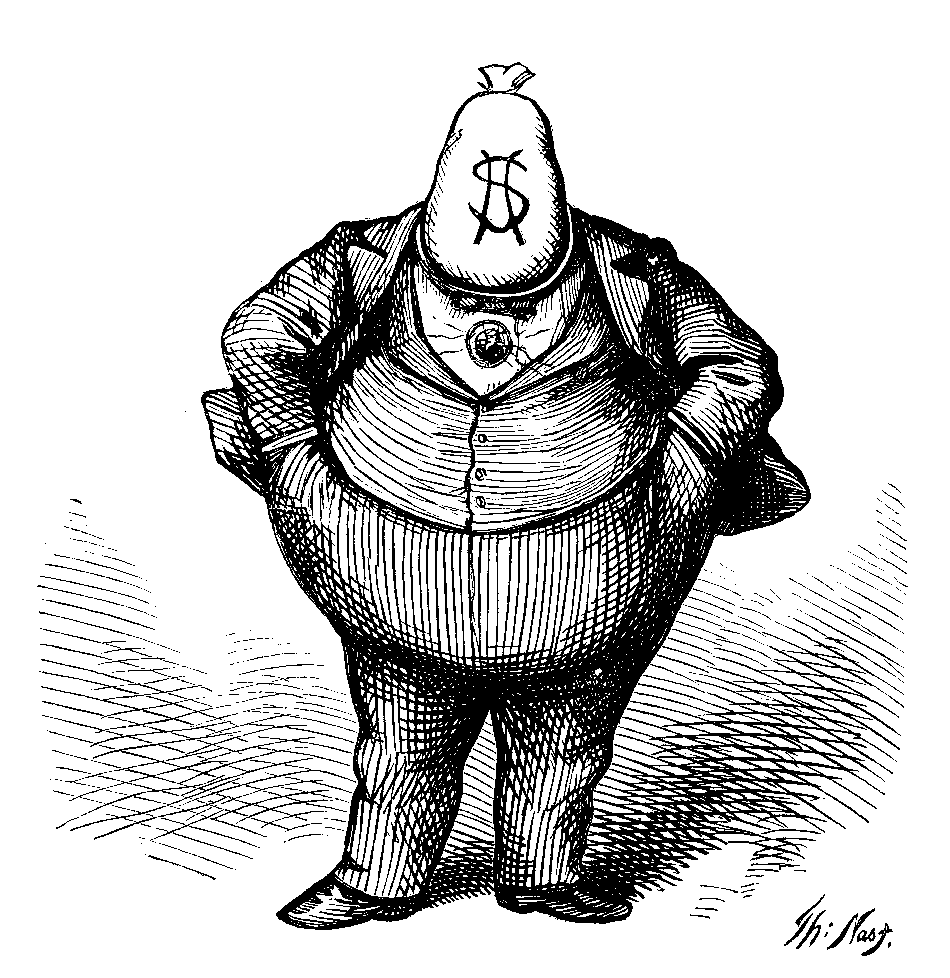

At ninety-five, as a businessman and philanthropist, I want to call attention to little-known ploys in US philanthropy that rob our society of hundreds of millions of dollars earmarked for important charitable causes—leaving money stashed away in financial institutions and doing no good for anyone except money managers and other financial intermediaries.

In the past twenty years, I’ve given away close to $500 million of my own money. After I pioneered the leveraged buyout in 1964, I watched how innovators, imitators, and swarming incompetents tore the companies they acquired apart. Then when I graduated into what I like to call my “distributive phase,” I saw how private foundations were able to take unfair advantages of the charitable deduction.

Writing in The New York Review back in 2003,1 I explained how a donor gets a tax deduction for all of the money put into a private foundation, yet the foundation is required to spend only 5 percent of its assets per year. That doesn’t mean “donate 5 percent to charity”—it means the 5 percent can be used for “administrative costs.” And I’ve commented on how these administrative costs may include generous salaries for family members and lavish all-expenses-paid tours to foreign countries for board members and administrators, all in the name of “research.” A recent article by Pablo Eisenberg in The Chronicle of Philanthropy disclosed payments made by the Otto Bremer Foundation to three of its board members amounting to over $1.2 million.2 Operating charities like the New York Public Library and the Metropolitan Museum of Art, on whose boards I serve, pay no trustee fees.

Recent estimates indicate that at least $700 billion is tucked away in private foundations, money that could be doing good for charities and for the economy—and you and I as taxpayers have underwritten the tax benefits awarded those foundations.

I’ve been angry about this for years. I’ve expressed my frustration in these pages, in The Wall Street Journal, and in interviews, and will continue to do so. But now I want to complain about a newer wrinkle that makes me even more indignant, one I deem “philanthropic gamesmanship.”

The more aggressive game in philanthropy I have in mind, one with a soothing but misleading name, is called Donor-Advised Funds (DAFs). Back in 1991, the Boston-based Fidelity Investments applied to the Brooklyn IRS and got a ruling that drastically changed the tax landscape governing charitable donations. Donors get the same tax benefits when they give to a DAF that they would get by contributing to a museum, soup kitchen, university, or any other federally accepted charity. But rather than having the gift made directly to a charity, the funds can simply sit in the account awaiting instructions from the donor. If the donor never gets around to making distributions, they stay in the account earning substantial fees for investment managers. Recently, mutual fund management companies such as Fidelity, Vanguard, and Charles Schwab have set up separate charity accounts to compete for funds.

These funds can provide such tax benefits because the donor must give up all legal control over his or her money when the transfer is made to a DAF. The control is transferred to the administrators of the DAF. Here’s a good example of what can happen. I’m a considerable supporter of a major cultural institution, and on its board of trustees. That institution had been receiving a sizable donation each year from a particular donor. When that donor had died, he had given his money to a DAF administered by a community trust. When the institution in question paid a call to the community trust, seeking confirmation about the continuation of the annual donation, it was told, “We’re not necessarily continuing to give that gift.” Note the use of the word “we”—nothing to do with the past practices of the late donor.

The 1969 Tax Reform Act set the rules for private foundations, but at that time there was no mention of DAFs. Professor Ray Madoff at Boston College Law School has long argued for laws that require timely payouts from DAFs; she says that there is now more than $60 billion tied up in them, and that the amount of money involved is growing at a high rate. Rather than the American people benefiting, it’s Fidelity and others who are thriving.

Professor Madoff is hosting a symposium on this and other topics at the “Convention on Promotion of Meaningful Reform in Philanthropy” in Boston this September 18–20. I plan to attend, and hope the conference will concentrate attention on ways to improve the system of charitable contributions.

It should be obvious that many operating charities can put to good use the huge sums now stagnating in banks or DAFs. Before I hit one hundred, I’d like to see all money designated as “charitable”—which the American government and its people underwrite through tax deductions—get into the hands of those who really need it. There should be a simple, uncomplicated bill relating to foundations and DAFs, fair and easy to understand, requiring that donated money not come under the control of profit-making financial managers. I urge all those who believe that charitable donations can make a difference in this world to make sure that tax-deductible gifts be given to operating charities in a timely fashion.

Advertisement

This Issue

September 25, 2014

The Cult of Jeff Koons

Obama & the Coming Election

Failure in Gaza

This Issue

September 25, 2014

The Cult of Jeff Koons

Obama & the Coming Election

Failure in Gaza