Chiseled over the entrance to the US Supreme Court are the words “Equal Justice Under Law.” The principle is foundational for a democracy. In 1974, when Richard Nixon faced the threat of impeachment for financial corruption and schemes to undermine democracy, he was forced to resign, and several of his top aides went to prison. There was broad celebration that the political system worked—that no one was above the law. “When the president does it…it is not illegal,” Nixon later claimed, but American presidents do not enjoy the privileges of kings and despots.

Half a century later, Donald Trump and most of his cronies could well enjoy impunity for actions even more corrosive of democracy and the rule of law. While in office Trump abused his pardon privilege to excuse dozens of corrupt, convicted allies, and he would likely do so again if reelected. We live in an age of selective application of law, in which influential people often evade responsibility for actions that are or should be criminal, while minor offenders such as shoplifters or drug users can face prison terms. Trump made crudely personal what has become tacit and structural.

In a dictatorship, the leader enjoys impunity and confers it on business allies—but crushes them if they show disloyalty. In both China and Russia, corruption is tolerated for supporters of the regime, but billionaires who express dissent abruptly find themselves charged with crimes. Impunity is fundamentally inconsistent with democracy.

A good deal of impunity reflects social class and privilege. For eons, powerful men have been able to have their way with women. The Me Too movement has worked to hold men accountable, with some notable, high-profile successes. But because of the legal ambiguity of too many sexual situations, impunity for sexual coercion is still more the rule than the exception.

For centuries, whites could function as absolute despots on plantations. After slavery ended, they could lynch innocent Blacks with no fear of legal retribution. Today, African Americans ostensibly enjoy the same civil rights as whites, but in practice Blacks are far more vulnerable to brutalization by police officers. The continuing insulation of police from the consequences of illegal acts is the epitome of impunity.

Anatole France wrote that “the law in its majestic equality, forbids rich and poor alike to sleep under bridges, to beg in the streets, and to steal their bread.” But there is a difference between the law in a capitalist system being systematically biased to discipline the poor while favoring the rich and impunity as the outright evasion of responsibility for criminal acts.

During and after the financial crisis of 2008, the degree of structural impunity in the US was pervasive and startling. Fraud was widespread. In the subprime collapse, investment bankers could underwrite securities backed by highly risky mortgage loans that they knew were likely to go into default. The greater risk produced higher yields. The safety of the securities, which were sold off to pension funds and other investors, was certified by unregulated credit-rating companies that were in cahoots with the investment bankers: the sponsors repackaged large numbers of mortgage-backed securities whose underlying collateral was junk, and the friendly credit-rating agencies blessed them as triple-A. But other than Bernie Madoff (whose larceny was an old-fashioned Ponzi scheme unrelated to the broader corruption), no senior financial executives went to jail. They enjoyed impunity because most of the conflicts of interest and bogus financial products that brought down the system were not technically illegal.

Why was it all legal? Because these same financial houses could translate their great economic power into political power to make the rules. Instead of heeding the urgent warnings of a few prophetic and marginal voices such as Brooksley Born, then the chair of the Commodity Futures Trading Commission, the Clinton administration forced Born out of office and in 2000 further deregulated credit derivatives, stimulating more abuses. A key architect of this deregulation was Clinton’s chief economic policy aide, Robert Rubin, who personally benefited from these weakened rules when he returned to Wall Street shortly after leaving public office.

With the criminal prosecution of Sam Bankman-Fried, the founder of the cryptocurrency exchange FTX, impunity for financial crimes may have reached its limits. Bankman-Fried tried to buy political influence, but he committed frauds at such a scale and with such flagrancy that his crimes were impossible to ignore, even for a system accustomed to indulging financial misdeeds. It remains to be seen whether the criminal prosecution of Bankman-Fried is a one-off, like Madoff’s, or the beginning of a road back toward the impartial application of the rule of law.

In Impunity and Capitalism, Trevor Jackson, a young economic historian at George Washington University, traces the contemporary dynamics of impunity for what ought to be financial crimes to the early history of banking and stock trading. Jackson’s core insight is powerful and original. Impunity for financial crimes was functional for the development of early capitalism, with echoes to this day.

Advertisement

This evolution in the law and practice of early capitalism was something of a paradox, because impunity for financiers came at the expense of investors. Before around 1720, merchants and their customers needed basic guarantees of property rights and the enforcement of contracts to facilitate commerce. But as the rudimentary commercial system evolved into the modern capitalist system of banks, stock underwriters, and corporations, entrepreneurs also needed to be able to take risks and impose losses on investors without facing economic ruin themselves. So the line between what was illegal and what was merely speculative shifted in the direction of buyer beware. A periodic financial collapse, with broad losses but no legal consequences for the promoters, was an acceptable price to pay for a dynamic system. “Impunity—the ability of some privileged actors to get away with causing harm—is a core feature of modern financial capitalism,” Jackson writes.

This shift paralleled the evolution of absolute monarchies into constitutional ones subject to the rule of law. In the period before modern capitalism, Jackson writes, financiers who were caught committing misdeeds could expect punishment. Their crimes, even if directed at others, were personal affronts to the Crown. If the king occasionally opted for random acts of mercy, that was also personal. “In the early modern period, impunity was an ad hoc privilege doled out by the sovereign; today, impunity is something built into the market itself,” Jackson writes.

In 1659 Louis XIV’s chief finance minister, Nicolas Fouquet, was convicted of misuse of public funds, including personal appropriation of the Crown’s money. Fouquet had his property confiscated and spent the rest of his life in prison. Between 1665 and 1716, Jackson finds, monarchs and their appointed judges typically held financial scoundrels accountable for their misdeeds. In France, for instance, more than four thousand financiers were fined during this period, and “some were sentenced to labor in the galleys.”

But as capitalism became more systematized, all kinds of speculations and deceptions were treated as perfectly legal. Capitalism needed entrepreneurial financiers more than it needed sure punishment for fraud and deception. In Jackson’s telling, if the system treated abuses too harshly, it would discourage risk-taking. The periodic collapses that resulted were treated as everyone’s fault and no one’s.

In 1709 the richest man in Europe, Samuel Bernard, went broke. Bernard functioned almost like a modern central banker. He borrowed heavily against his own credit and lent money to merchants and municipal governments all over Europe; his loans to the French state funded many of Louis XIV’s wars. Merchants and sovereigns also relied on Bernard to provide foreign exchange. “He would often obtain Spanish piasters for troops in Flanders who needed to be paid in local guilders,” taking a commission on both sides of the transaction, Jackson writes.

When Bernard became overextended and defaulted on his debts, it created a general credit contraction in much of Europe and destroyed the finances of several municipalities. “For months, it was impossible to find anyone willing to lend money at any price,” Jackson tells us. But so intricately was Bernard connected to the financial system that it was not in the interest of the regime to destroy him. After briefly fleeing France, he was given time to restructure his debts, and received immunity from prosecution. In today’s parlance, Bernard was “too big to fail.”

Thus began an era of increasing impunity, in which speculation, conflicts of interest, and deception of investors were seen merely as normal aspects of the emergent financial system, not as crimes. “After the death of Louis XIV” in 1715, Jackson writes,

the duc de Noailles, the hapless new controller general of the finances, was left to grapple with the enormous debts left over from Louis’s wars, and part of his solution was the establishment of a chambre de justice.

The idea was to create a special court to make an example of reckless bankers and divert attention from the Crown’s own irresponsibility. The edict creating the chambre defined a new type of financial criminal, agioteurs (speculators), who were to be punished for the crime of rigging markets and speculating at the expense of the general public. But the gambit failed. The chambre of 1715–1717, Jackson reports, was the last one ever held.

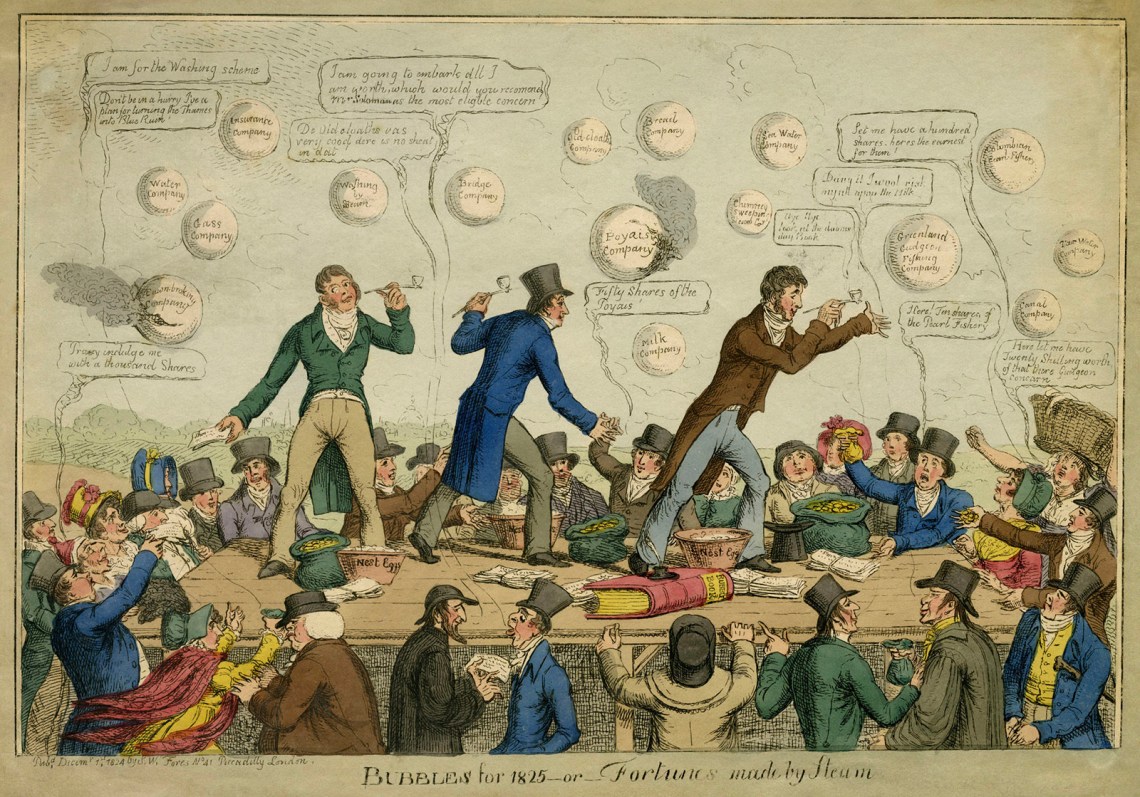

By about 1720, impunity for all but the most fraudulent speculations was well entrenched within the emergent financial and legal system. In that year two notorious financial bubbles, the South Sea Bubble in England and the Mississippi Bubble in France, enriched promoters and created catastrophic losses for other investors and for the economy. Both bubbles were intimately connected to colonialism. The Mississippi Company was chartered to promote the creation of French settlements in North America. The South Sea Company was granted a royal monopoly to provide slaves to South America.

Advertisement

The twin crises of 1720 combined a stock market collapse, a currency crisis, and an early episode of hyperinflation. Despite an inquiry by the British Parliament and the disgrace of some politicians who had been bribed, the companies’ promoters and beneficiaries largely evaded prosecution. The elaborate schemes—in which sponsors of the speculations engaged in insider trading, deceived investors, and unloaded securities on them—would be familiar to the investment bankers who created the 2008 subprime crisis.

As capitalism developed, financial impunity was also facilitated by liberalized bankruptcy laws, first created in Great Britain during the reign of Queen Anne. Prior to 1706, a bankrupt person who failed to pay his debts could languish in debtors’ prison indefinitely. That year, a statute was enacted in response to widespread economic ruin caused by plagues and wars that had destroyed much of the merchant class. Under its terms, a magistrate appointed by the Crown could settle a merchant’s unpayable debts at a discount of so many pence in the pound, and the merchant could be freed to resume his commercial and personal life. Those who couldn’t settle their debts remained in prison. Generous bankruptcy protections in the US and the UK still exist for corporations, which can go before a judge, reduce or wipe out past debts, and carry on. However, an individual who declares personal bankruptcy typically faces economic ruin.

By the late eighteenth century London had become a center of global finance, underwriting myriad worldwide stock and bond issues. In the early nineteenth century, lending to the newly independent nations of South America at high interest rates became a London investment fad. Many of these loans financed highly risky mining ventures in which local power brokers had personal interests. The bankers who profited from promoting these sovereign bonds did not exercise “due diligence,” as we would say today. Nine nations—including Colombia, Peru, and Chile—went bankrupt in the 1820s, failing to pay their debts. In turn, more than a hundred bankers in England and Wales failed, costing their investors fortunes and creating a credit crunch.

Corruption greased the system. “Of the 278 directors of Latin American mining companies, 45 were [British] MPs,” Jackson tells us. Despite extensive fraud and conflicts of interest,

nobody was prosecuted for anything, nor was there any indication or suggestion that anybody should have been….

Somehow, between about 1690 and about 1830, financial crises stopped being crimes and became natural disasters.

One famous swindle in 1823 involved the sale of securities in London markets for a fictitious Central American nation named Poyais. But as Jackson astutely points out, Poyais was only slightly more fictitious than actual territories and countries such as British Honduras (today Belize) or, later, Panama, which were created by explorers armed with royal charters or gunboats. Gregor MacGregor, the sponsor of the Poyais fraud, hoped to create a real colony if he could raise the money. “MacGregor was able to exercise a certain kind of impunity in the context of colonial land grabs and war profiteering,” Jackson writes. Thus did the impunity of early capitalism and the impunity of colonialism reinforce each other.

Jackson’s account is well worth reading because of the power and continuing resonance of his central insight—impunity facilitated capitalism. The book is uneven and frustrating in some respects. Jackson writes that before the early eighteenth century, “impunity was personalized: the prerogative of sovereign authority, granted individually on an ad hoc or even arbitrary basis.” This generalization sounds right, but he gives hardly any examples. And we jump from a cogent discussion of impunity in the crises of the 1720s to a convoluted section on the development of central banking, drawn largely from an unrelated journal article of Jackson’s, that scarcely touches on the question of impunity, and then back to impunity in Britain in the 1820s.

Jackson’s details occasionally contradict his narrative. In his telling, monarchs enjoyed impunity, which they could randomly share or deny to others who broke the law. But that account needs to be qualified. Supposedly absolute monarchs, such as the French and British kings of the period before 1700, were in fact far less than absolute. Under feudalism, kings were constrained by the rights of lesser lords, the power of the church, and legal protections for merchants under the Lex Mercatoria, which guaranteed property rights in cross-border commerce. The ideas that informed the Declaration of Independence and the Constitution of 1789 can be traced to constraints on British monarchs dating back to the 1680s. Jackson himself describes one episode involving a maneuver by Charles II to default on over £1 million of sovereign debt at the expense of bankers who had lent the Crown the money. But as Jackson recounts, the bankers sued, first in the Court of the Exchequer in 1691, and won a final judgement that the king could not override in 1700, in the House of Lords, which functioned as Britain’s final appellate court.

In this book, the reader has to work hard to distinguish the signal from the noise, and yet the noise is invariably interesting in its own right. Despite such blemishes, Jackson is a diligent researcher; his findings are worth knowing. And they indeed foreshadowed and shaped the events of the twentieth and twenty-first centuries. Jackson ends his story in the early nineteenth century, but the pattern of impunity for financial deceptions continued. The growth of a financial system marked by impunity paralleled the rise of other legal inventions that protected capitalists when their schemes misfired. The limited liability corporation became widespread in the US after 1811, when New York enacted the first law permitting manufacturing entrepreneurs to get corporate charters at will rather than requiring special legislation for each one. The LLC allowed entrepreneurs to risk only the money they had invested and evade responsibility for other losses or liabilities if the company went broke. By selling shares to others, they might even cash out their own stake and offload risk onto the buyers—exactly what modern investment bankers do. In the absence of gross fraud, it’s perfectly legal.

In the nineteenth century both statutory law and the common law were constructed to give a company almost total immunity from reckless actions that harmed employees, on the convenient premise that the worker’s decision to take a job was a voluntary contract, even though the employer had total control over the terms. This doctrine, reflecting both free-market dogma and the political influence of elites, entirely assumed away the imbalance of economic power. Similar prejudices held sway in tort law. In Winterbottom v. Wright (1842), a landmark English case that influenced both British and American common law for the better part of a century, a coach driver employed by the postmaster general to carry mail sued the contractor responsible for keeping the coach in good repair for negligence when the carriage broke down and the driver was injured. But the Court of the Exchequer held that because the driver had no direct relationship with the contractor, he could not sue.

What is striking about each of these mechanisms is the double standard. As in the case of bankruptcy, the law favored employers over workers. Not until the Progressive Era in the US did courts and legislatures in a few states recognize the plain imbalance of economic power and begin to hold employers accountable and give workers some avenues for remedy.

Even with the creation of the US Federal Reserve in 1913, periodic credit collapses and stock market crashes continued to occur. Just as Jackson suggests, they seem inevitable features of a market economy—the fault of everyone and no one. A number of twentieth-century economists, including John Maynard Keynes, Charles Kindleberger, and Hyman Minsky, have described how capitalism, absent strong regulation, is systemically vulnerable to financial bubbles followed by crashes. Speculators become overextended; financial fads turn out to be wishful. When investors try to cut their losses and sell, there are too few buyers, the values of securities collapse, and the losses in the financial economy spill over and deny needed credit to the real economy.

That pattern seems to apply to most of modern history, with the one notable exception of the period that began in the 1930s and persisted for at least thirty years. In that era financiers were held accountable, sometimes criminally, for fraudulent acts. Under the newly enacted laws of the New Deal, banks, stock exchanges, brokers, and investment bankers were more tightly regulated than in any era before or since. In 1938 Richard Whitney, the president of the New York Stock Exchange from 1930 to 1935, was convicted of embezzlement and served three years at Sing Sing. Charles Mitchell, president of National City Bank, admitted to peddling shoddy investments to bank clients and personally paid a $1 million fine.

But the main achievement of the tough regulation of that era was not the number of bankers punished but the abuses avoided in the first place. Far from hobbling capitalism, the passing and enforcing of laws against deceptive financial acts was salutary for the market economy. Once the New Deal rules were in place, there were no stock market collapses for half a century and hardly any bank failures. Both resumed after the rules were weakened. It turned out that impunity was not a necessary condition for financial capitalism, just the norm—and a great convenience for capitalists. It remains to be seen what it will take politically to restore greater accountability to capitalism.

Though Jackson ends his saga two centuries ago, it is a prologue to our own era. Recently Jackson has been writing critically about cryptocurrencies, a twenty-first-century realm of financial abuse (and impunity for promoters who deceived customers) that chimes perfectly with his findings about the eighteenth century.* Writing before the FTX collapse, Jackson presciently observed:

Promoters of cryptocurrencies and blockchains claim that they offer an escape from, or an alternative to, the impunity of financial capitalism. Instead, they have shown why finance in general needs to be subject to democratic control and public accountability.

It would be premature to conclude that the fall of Trump, Bankman-Fried, Harvey Weinstein, and a very few others heralds a new turning away from impunity. On the contrary, impunity for corporate executives remains the norm. During the three years leading up to the pandemic, Southwest Airlines diverted $5.6 billion to stock buybacks to enrich executives rather than upgrade its systems. The result was a ruined Christmas holiday in 2022 for hundreds of thousands of travelers when more than 15,000 flights were canceled. There were no personal consequences for executives. Between February 2020 and December 2022, three different government agencies fined Wells Fargo a total of $7.2 billion for serial violations of law that fleeced customers, but no individuals were prosecuted. Then as this article was going to press, the Department of Justice announced a plea bargain with the senior executive in charge of the frauds, Carrie Tolstedt, which in principle could include prison time. Sentencing has been deferred.

In the 1930s it took a successful political revolution for the New Deal to end impunity for financial crimes—temporarily, as it turned out. There has also been serious backsliding from the civil rights gains of the 1960s. The implications of the movement for Black lives and the Me Too movement are revolutionary, but not the results. And democracy barely survived Donald Trump. Impunity is a useful mirror. It is not a flattering one.

This Issue

April 20, 2023

The High Cost of Being Poor

A Formative Loss

This Issue

April 20, 2023

The High Cost of Being Poor

A Formative Loss

-

*

See, for example, Trevor Jackson, “The Crypto Crisis,” Dissent, August 8, 2022. ↩